.png)

Last week, the European energy industry descended on Essen for the 25th edition of E-world energy & water.

Our team had a packed agenda at the event, meeting with buyers, developers, advisors and utilities from across Europe. If these discussions made one thing clear, it is that the market is shifting. With negative prices and cannibalisation sending shockwaves across European markets, the sector is clear-eyed about the challenges of 2026, but also moving confidently towards solutions.

Here’s a roundup of the big trends we are seeing in power markets that defined our conversations at E-world this year.

1. Hybrid and Combo PPAs are becoming essential for ensuring PPA value

A PPA which combines generation with storage, such as solar with battery energy storage systems, is a hybrid PPA. A PPA which combines different generation types, such as solar with wind, is a combo PPA. Both are becoming more sought-after options to mitigate negative price risk and reduce the impact of cannibalisation on PPAs.

Storage came up a lot during our conversations at E-world. Whether discussed as standalone battery assets or integrated alongside generation, market participants increasingly understand storage as an essential instrument to:

- Add a premium to PPAs by firming up intermittent supply

- Shape generation profiles to better match buyer demand curves

- Mitigate downside risk by shielding assets from the most volatile pricing hours.

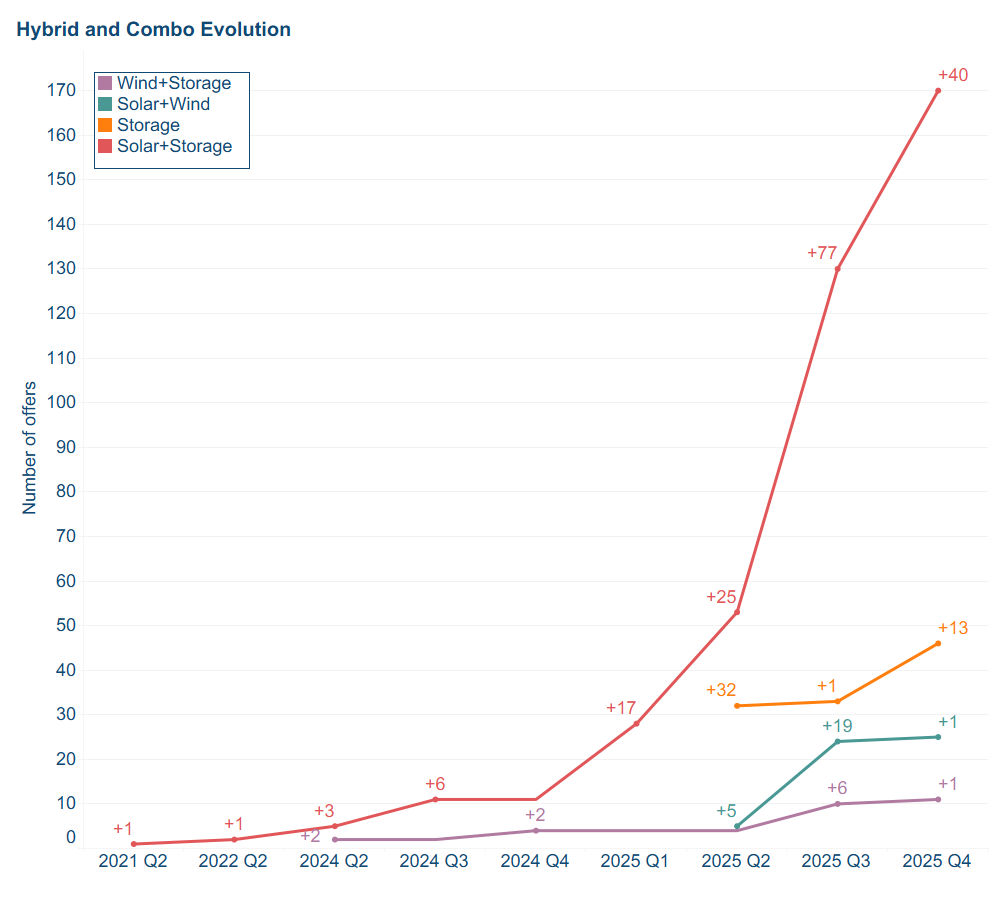

The graph below, which we revealed in a presentation at our stand to E-world attendees, shows the increase in storage offers on the LevelTen Platform in recent months. From a trickle of hybrid offers from 2022 onwards, we ended 2025 with over 170 hybrid offers on the Marketplace. These were spread across European markets, with countries that face elevated cannibalisation risk — such as Germany and Spain, with their abundance of solar generation — accounting for the lion’s share.

Standalone storage offers have seen an uptick in recent months, driven by a combination of market conditions and declining technology costs, while solar + wind combo PPAs are also seeing increased traction. These structures, which combine solar energy with the round-the-clock generation profiles of wind, can be used to provide more reliable baseload-like supply curves compared to solar alone. These offers can either be derived from physically co-located assets, or on geographically separate projects that are virtually aggregated into one contract structure.

PPA dealmakers looking to better understand the complex world of hybrid, combo and storage deal structures can find guidance on our website.

2. Scope 2 uncertainty is impacting procurement strategies

The ongoing updates to the Greenhouse Gas Protocol Scope 2 guidance were a major topic of discussion in our booth. While the final decision remains under consultation, the direction of travel is influencing how deals are being structured today.

There is palpable uncertainty regarding these changes, and their potential impact on the PPA market. Many buyers we spoke to are prioritising projects that are likely to align with stricter guidance, specifically focusing on:

- Granularity: sourcing data that supports hourly matching claims, should they become mandatory

- Locality: prioritising PPAs within the same bidding zone as their demand, reducing cross-border accounting risks.

While the sector awaits further clarity around these proposed changes, and whether grandfather clauses will be applied to deals signed today, PPAs continue to provide a valuable economic hedge against price uncertainty that protects buyers from future price volatility.

3. We see strong appetite for more structured products

Despite market challenges, the atmosphere among buyers and sellers is cautiously optimistic, with a strong appetite to get deals signed.

Corporate buyers are eager to secure long-term value. Developers are meeting this demand with viable, sophisticated projects and a range of deal structures that address the risks of a mature renewable grid. With market conditions reducing the market demand for pay-as-produced PPAs, buyers are increasingly seeking structured solutions where generation aligns better with the demand-side consumption profile. These structures are hard to find, price and compare; LevelTen can help.

E-world 2026 proved that, while European energy markets grow more complex, dealmakers are getting more ambitious. The tools, the technology, and the capital are all present to accelerate the next wave of clean growth and power the energy transition forwards.

4. Data makes the difference

With ongoing cannibalisation pressures and negative price pressure across Europe, having access to robust, reliable data is essential.

For developers, ensuring projects make it to RFP shortlists while maintaining positive revenue forecasts is key — here's more on that. For buyers, closing deals involving complex deal structures and sophisticated contractual clauses means being confident in your numbers. That's where LevelTen comes in, as the industry's only provider of up-to-date price data based on real corporate PPA offers.

LevelTen is the leading provider of transaction infrastructure for the clean energy transition, connecting buyers, sellers, and financiers through dynamic marketplaces, data-driven insights, and automated analytics.

Interested in exploring how advanced PPA procurement strategies can benefit your organisation? Contact info@leveltenenergy.com to learn more about our platform and solutions.

.png)