The lowdown: Europe's rapidly growing clean energy sector is facing challenges from price cannibalisation and curtailment, which suppress revenues for developers and complicate PPA procurement for buyers. These market dynamics signal a shift away from traditional pay-as-produced solar PPAs. To mitigate risk and secure financing, the market is broadly moving towards multi-technology, structured PPAs that provide enhanced risk protection.

Europe continues to make significant progress in integrating renewable energy sources into its power grid. In 2025, wind and solar generated 30% of the EU’s electricity, surpassing fossil-derived power for the first time on record.

Europe’s solar success has helped to progress decarbonisation goals and lower energy prices. Nonetheless, the growing pressure of midday price cannibalisation is suppressing capture rates for PV in many markets, undermining project economics. It is clear that, for solar energy to continue its key role in advancing the energy transition, battery storage energy systems (BESS) will be essential.

For storage, whether standalone or co-located with solar, hybrid PPAs provide an efficient route to market.

A shift away from standalone solar PPAs?

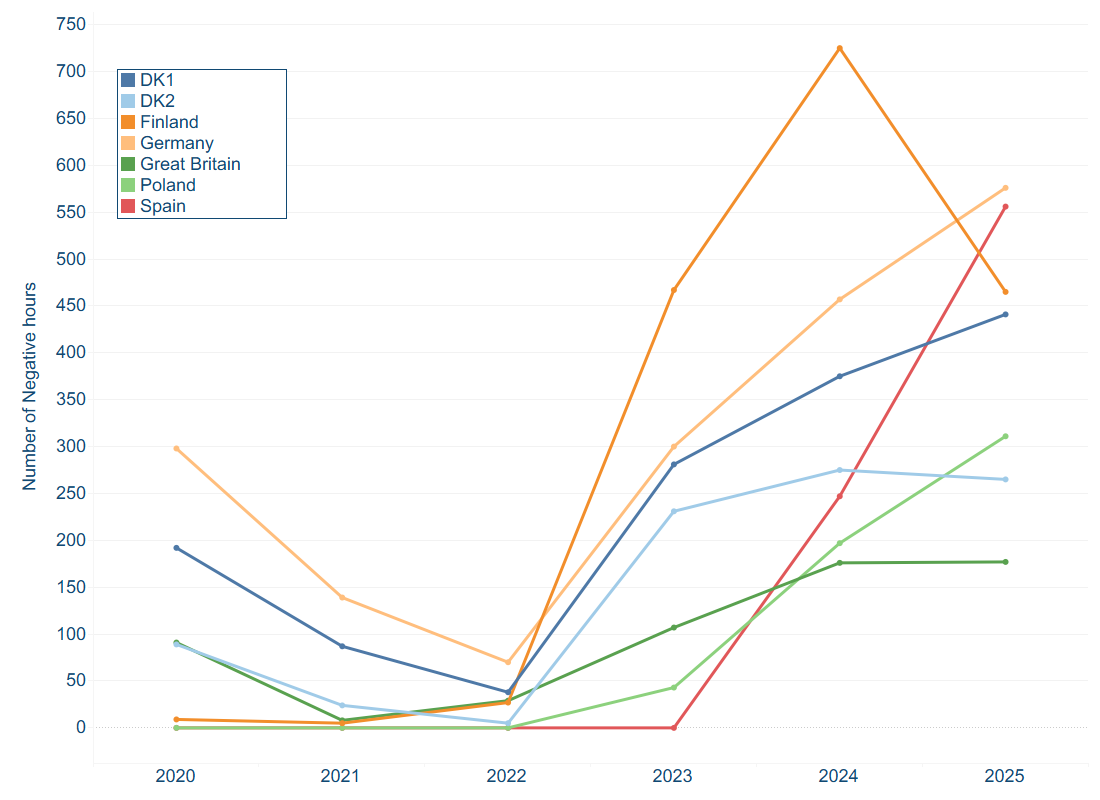

Midday price cannibalisation is caused by high levels of solar generation, but it can be exacerbated by a variety of factors. In countries with high amounts of inflexible generation, such as nuclear-heavy Finland and coal-dependent Poland, plants often continue to operate during negative-price hours regardless of market conditions (it is expensive to wind down a nuclear reactor!). In other markets, inflexible subsidy schemes create the same effect by incentivising renewable energy producers to keep assets online. After all, if the payments and/or Guarantees of Origin (GOs) keep coming, why stop producing?

Due to the highly integrated nature of the European grid, these price-suppressing effects are not limited to the countries where the phenomenon is most acute; spillover effects are also manifesting in neighbouring markets. Portugal often imports negative prices from Spain; the island of Ireland, with its limited interconnection to other markets, is largely protected.

The graph below reveals the proliferation of negative price hours in Europe during recent years.

For energy sellers, cannibalisation means suppressed revenues and greater difficulty securing the financing they need to build in the first place. For buyers, it can disrupt the financial viability of long-term contracts, and negatively impact the cash value of their existing PPAs.

Suppose wholesale market capture prices drop below the strike price of an organisation's PPAs. This scenario can make the buyer's business case for getting new agreements signed challenging, adding difficulty to the process of securing approval from corporate finance departments. Dynamics such as these can place the high-quality, additionality-backed GOs that corporate sustainability leaders need to reach their goals further out of reach.

Unsurprisingly, the market is responding. While traditional solar PPAs continue to provide compelling offtake opportunities for energy buyers across many markets (especially those in regions markets with low cannibalisation rates and/or limited availability of local clean energy certificates), negative price concerns are moving the numbers on these agreements more broadly.

In many markets, the era of pure-play, pay-as-produced solar PPAs is giving way to more sophisticated hybrid PPAs that leverage the performance benefits of battery storage.

Our next blog will dig deeper into how batteries are plugging into the mix.

Got questions? Connect with Andrés via LinkedIn or reach out to our team.

.png)