The July 4 tax credit cliff is swiftly approaching. It’s been nearly a year since the Trump Administration’s One Big Beautiful Bill Act (OBBBA) passed, bringing a premature end to tax incentives for solar and wind development. Savvy clean energy buyers recognize that the window to lock in financeable projects at today’s pricing is narrowing fast.

What’s led up to this moment?

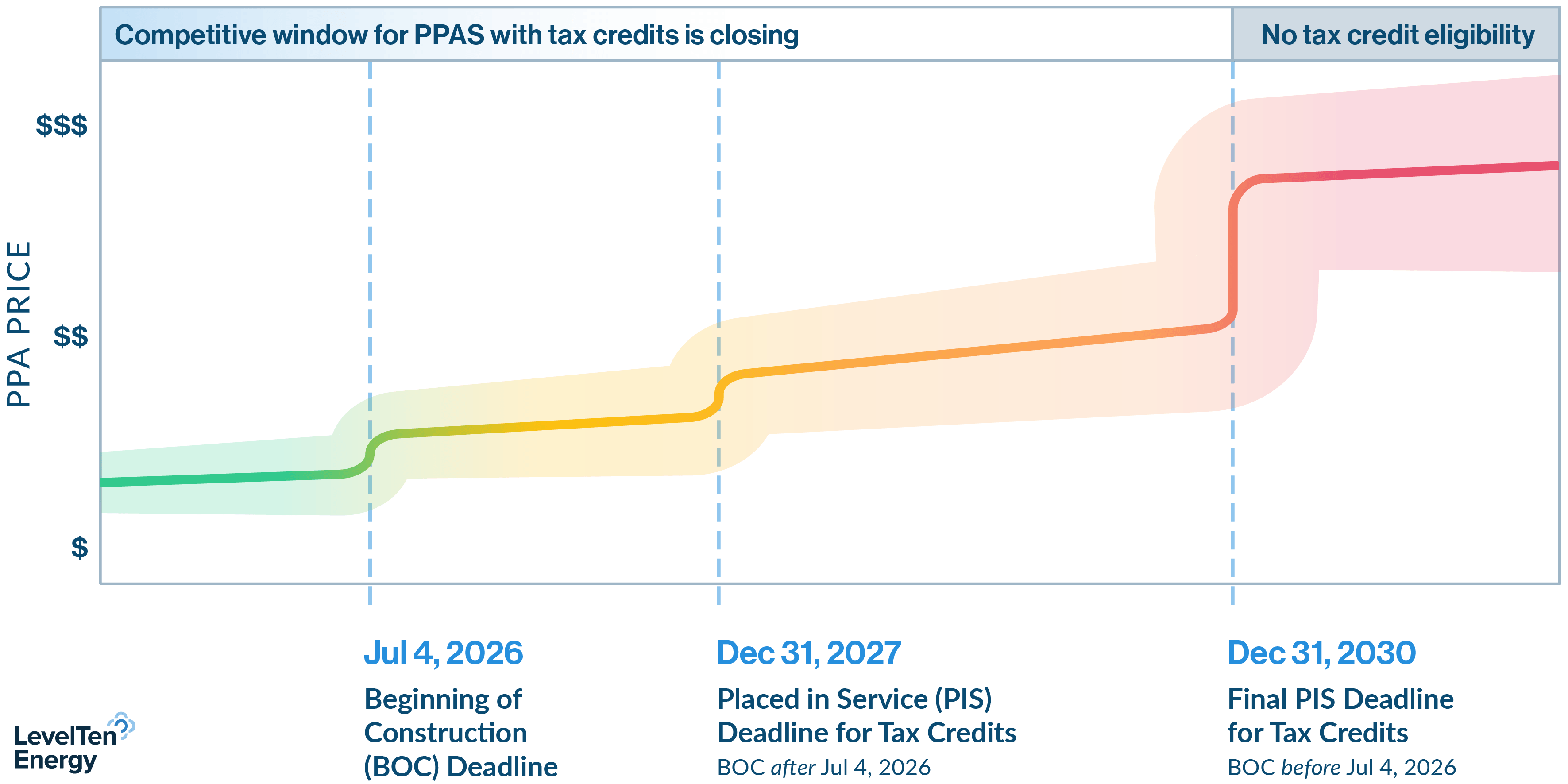

Among the OBBBA’s many provisions was a fundamental restructuring of federal tax credits. The law called for utility-scale wind and solar projects to either begin construction by July 4, 2026, or be placed in service (PIS) by December 31, 2027, in order to qualify for federal tax credits. A recent US district court decision to uphold the alternative construction-start test of “5% of total project cost incurred” may give developers one more route to claim tax credits, but uncertainty around actually leveraging this approach within a very tight timeframe will likely limit its use. All projects, regardless of construction start date, must achieve PIS by December 31, 2030 to qualify for tax credits.

Now is not the time to wait on the sidelines.

After July 4, 2026, the pool of projects with tax credit access freezes. Barring a remarkable policy reversal down the road, no new projects beginning construction after this date can realistically qualify. Over time, this means the supply of tax-credit-eligible projects will dwindle, the market will see more buyer competition for a shrinking pool of viable assets, and, most importantly, PPA prices will rise as pricing leverage shifts from buyers to sellers. Ultimately, there is a fixed number of fully safe-harbored, renewable energy projects available on the market. Once they’re gone, they’re gone.

Active buyers understand the immense value of developmentally mature, safe-harbored projects in today's market environment. Since last July, 50% of the projects on our original “Most Valuable Projects on the Market” list are no longer available.

Supply is shrinking by the week, and prices are expected to be on a one-way trajectory upward into 2028 and beyond. The good news is: there are still compelling, tax-credit-eligible projects available — and LevelTen can help you find them.

What Does The Market Look Like Now?

Quick takeaways:

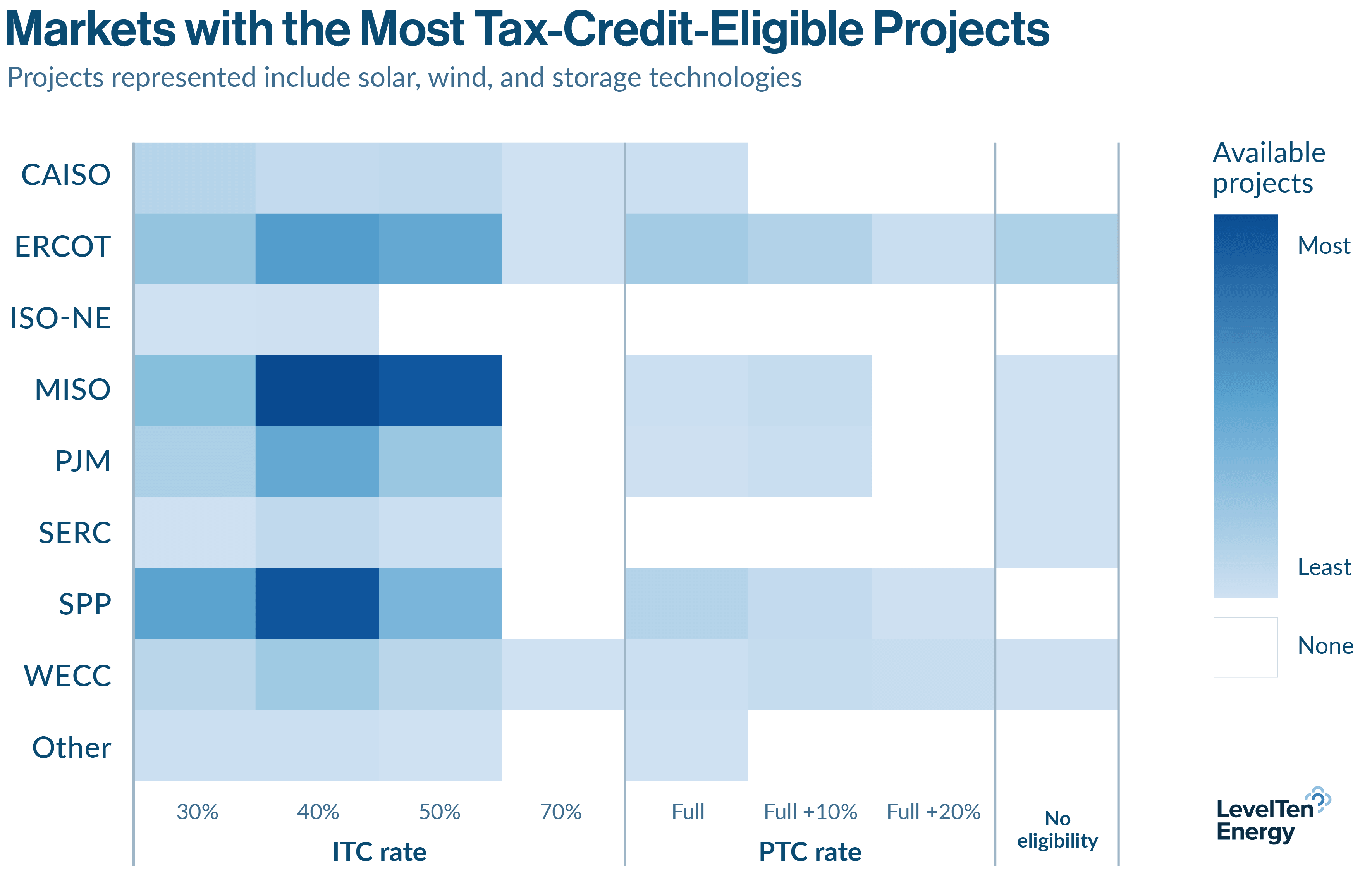

- Most developers are targeting one, if not two bonus adders

- MISO and SPP are hot spots for tax-credit-eligible projects across technologies

- SPP has a notable PTC presence driven by wind projects

- ERCOT has strong ITC and PTC representation reflecting its solar and wind mix

Where do PPA prices go from here?

In our initial September 2025 analysis, we saw PPA price offers for the most attractive projects increase up to 7% in just three months after the OBBBA’s passage. And as the pool of tax-credit-eligible projects dwindles and competition for supply intensifies, prices will continue to rise.

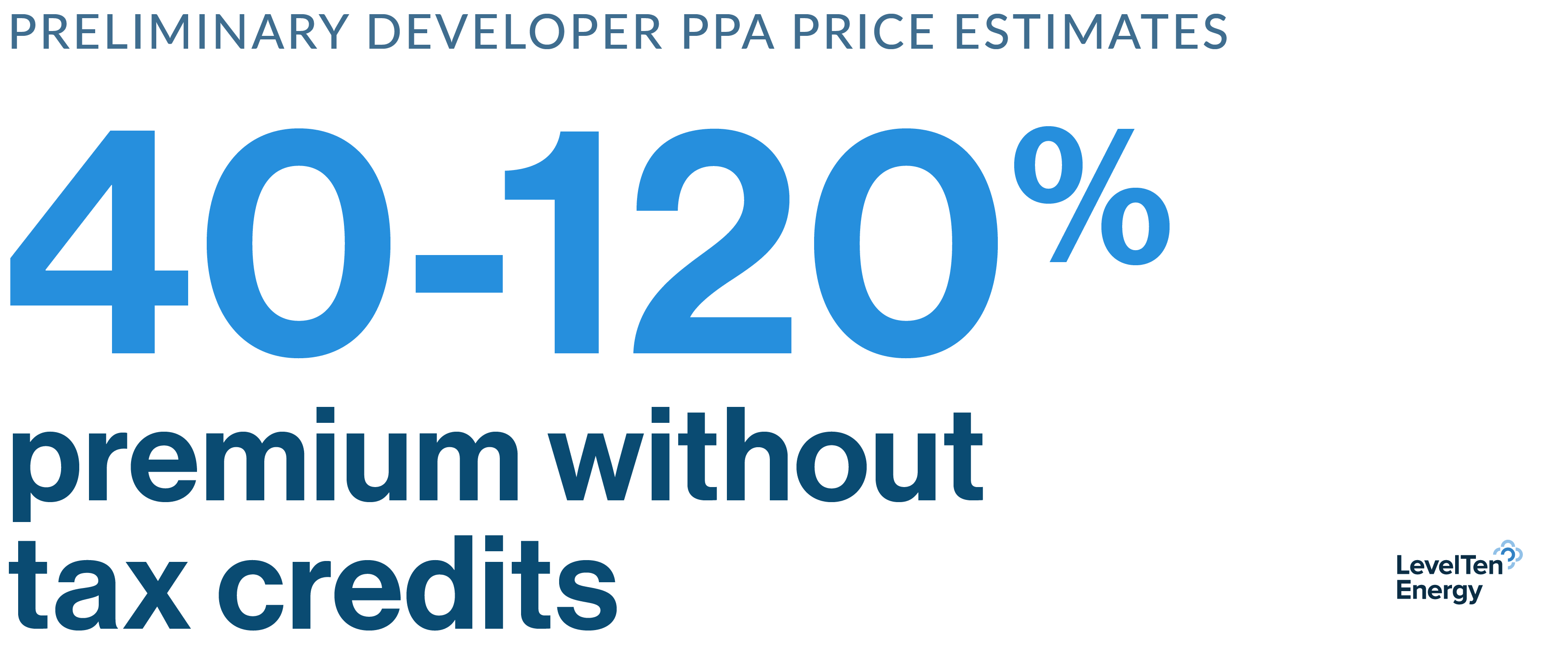

Real-world insights on PPA prices without tax credits have been nearly nonexistent since the OBBBA's signing as developers continue focusing their origination and marketing efforts on safe-harbored assets. But glimpses have begun to appear. LevelTen has received pricing estimates from a handful of developers showing pricing assumptions with and without ITCs. There is a wide range, reflecting differing strategies and assumptions among developers. While some indicate a 40-50% increase in PPA prices across all ISOs, others are pricing much higher. For instance, early transaction data in ERCOT suggests that PPA prices couldmore than double without ITCs/PTCs — an increase of 120% or $66.21 per MWh.

A more precise view of PPA price changes will emerge as more developers begin to model projects without tax credits. But it is already clear that buyers who act now stand to lock in the best economics the PPA market can expect for the coming years. Contracting with a tax-credit-eligible project today means securing terms that reflect today's economics, before a no-tax-credit premium becomes the PPA market's new normal.

Where are the opportunities?

According to CEBA (Corporate Energy Buyers Association), more than 13 GW of clean energy has already been contracted this year. Yet, last year, the number of unique energy buyers dropped 40%. While part of this decline reflects data center developers and hyperscalers executing PPAs for financially attractive projects, data center development is typically constrained to specific geographies to secure accredited capacity or serve precise colocation needs. These constraints leave strong, tax-credit-eligible projects available for corporate PPA buyers, even in high-demand markets. Put simply, many large energy buyers may have a competitive advantage in areas where data centers plans are less sweeping.

The buyers who come out ahead in this market won't be the ones who waited for perfect conditions — they'll be the ones who recognized and acted upon today's favorable conditions. The tax credit window is closing, supply is tightening, and prices are moving in one direction. But today's economic opportunity is real, quantifiable, and still accessible to those who act with speed and intention.

Reach out now to access the updated list of the market's most attractive projects and learn how LevelTen can accelerate your procurement ambitions today.

.png)